Friday Finance: A Simplified Guide to IPOs

Here’s a high-level discussion framework that is meant to be clear and conversational. Think of it as a story with six chapters and some final thoughts.

Chapter 1. Why Does a Company Go Public?

Imagine that you have built a great restaurant that became a small chain. You need money to expand to 50 locations, which will cost more than any bank will lend you. One option is to consider an initial public offering. Going public means selling pieces of your company to thousands of strangers who believe in your future.

To add some heft to the restaurant side of the story, Jersey Mike’s (the submarine sandwich franchise), which has been private since 1956, has mentioned it will be floating their shares on the public market this year. Why, you may ask?

The core reasons companies go public:

- Raise growth capital — fund expansion, pay down debt, or invest in new products (many new restaurants) without borrowing (taking on MORE debt)

- Let early believers in your company cash out — founders, employees, and early investors have been waiting years for their reward. Going public creates a marketplace where they can finally sell their shares and diversify their holdings beyond the one company they run

- Currency for deals — public stock can be used to acquire other companies instead of cash

- Credibility and visibility — being publicly traded signals to the market that “you’ve arrived.” It helps attract talent, customers, and partners

The simple truth: Going public turns a private club into an open marketplace. After an IPO, anyone can own stock in a company. And those shares are bought and sold during trading hours for the rest of the company’s banking life.

Chapter 2. What Does It Do for Existing Stockholders?

Before an IPO, if you own shares in a private company, they’re essentially a piece of paper with a promise — valuable on paper, but you can’t pay your mortgage or buy a car with them.

Going public creates liquidity — the ability to convert that paper into real money:

- Employees who received stock options as part of their pay can finally sell them

- Early investors (venture capitalists) can return money to their own investors

- Founders can diversify their personal wealth instead of having everything tied to one company

Think of it as a real estate transaction. In this case you own a house in a neighborhood with no buyers. The IPO builds the road that lets people in. Suddenly your house has a real market value and you can sell it.

Another way to put it: an IPO is basically a company moving from a private club to a public marketplace. The company gains access to huge amounts of capital, founders and employees gain liquidity, investment banks organize the sale and earn fees, and the public gets a chance to become owners. The tricky part is figuring out a price that’s high enough to raise money but low enough that investors still want to buy. It’s a little like selling tickets to a concert—you want a full house, not empty seats, but you also don’t want to leave too much money on the table.

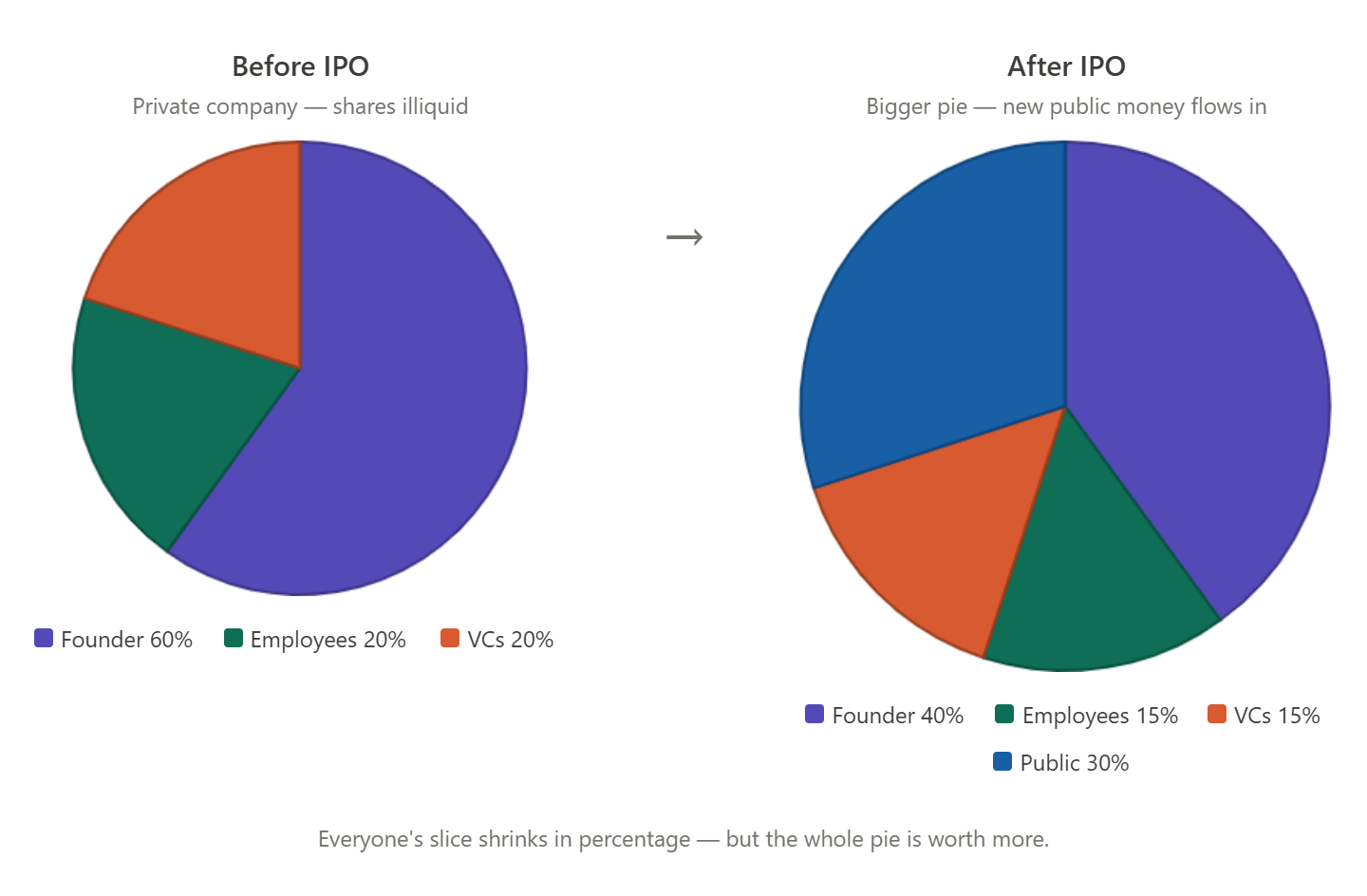

Another key feature of IPOs is that they change the capital structure of a company. As companies go from private to public, different dynamics come into play, particularly on the ownership stake of the participants. The percentages below are purely hypothetical, but serve as a fair example of the before and after look at the liquidity of the shares:

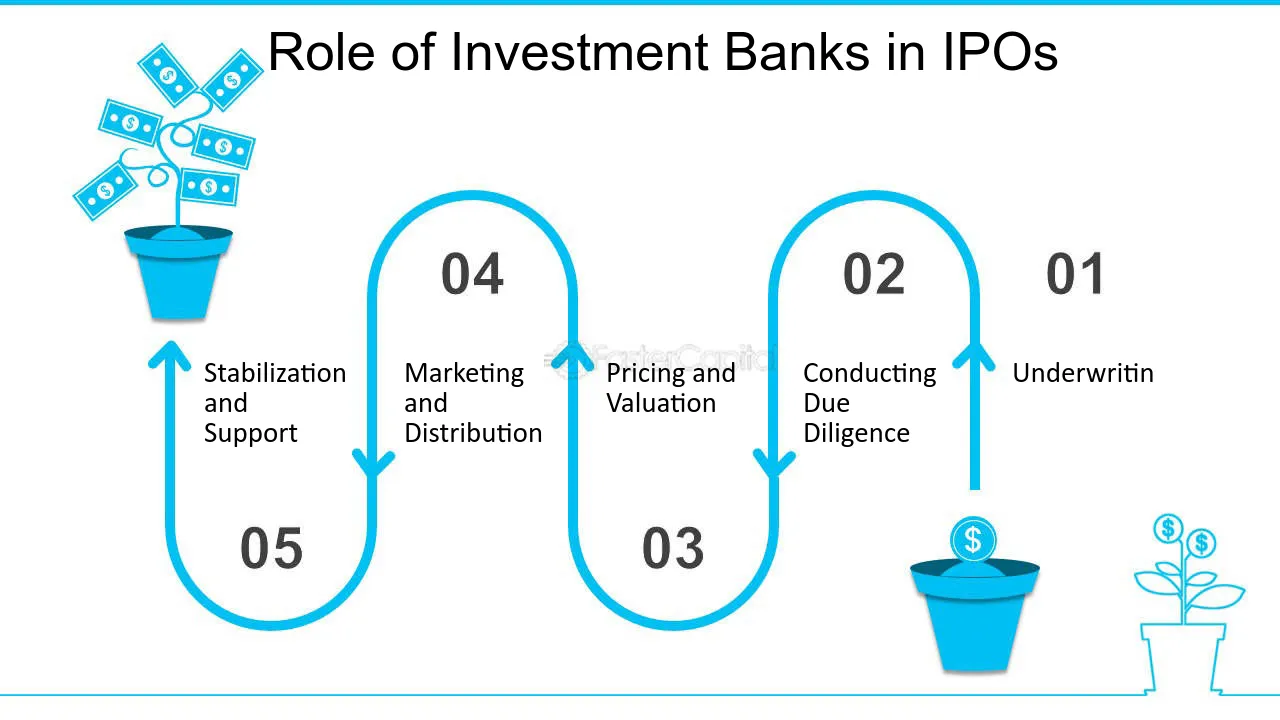

Chapter 3. What Do the Banks Get?

The investment banks (e.g. J.P. Morgan / Chase, Goldman Sachs, Morgan Stanley, etc.) act as the trusted middlemen who take the company to Wall Street. The arrangements, established by the SEC, are the same on the NYSE and the NASDAQ in the US. The investment bankers do some heavy lifting: valuing the company, writing the legal prospectus (the “S-1”), traveling the country pitching to big investors (“the roadshow”), and managing the actual sale (which includes buying any shares in an IPO offering that do not sell to the public).

Their compensation is called the underwriting spread — typically 5%-7% of the total money raised. On a $1 billion IPO, for example, that’s $50–70 million, split among the banks involved.

In plain terms: They’re like a real estate agent, except the house costs a billion dollars and they charge accordingly.

The SpaceX IPO, for example, established a valuation on the company at $2 trillion: in numbers that is $2,000,000,000,000! Let’s just say, the investment bankers made a killing. The stock holders? Well time will tell, but the original share price was pegged by the Investment Bankers at $135, however, the first shares sold at $150 in the first hours of trading and finished upwards of $225 over the next week. The first POP was significant, marking a rise of 67% from the IPO price. Since then it has had a large fall in price, down to approx. $125/share. But note: the public float is very thin, and when the upcoming insiders have their “lock-ups” expire that will put some additional downward pressure on the price.

How does this compare with typical IPOs?

This pattern is actually common among high-profile IPOs:

- Strong first-day “pop” in the stock price.

- Momentum buying pushes the stock even higher.

- After the excitement dissipates, the company’s stock price tends to fall back down to earth with a more realistic market value.

Chapter 4. What Is a “Green Shoe” and Why Does It Exist?

This is one of the most cleverly named expressions in finance. The green shoe (officially called an overallotment option) is a tool that helps stabilize the stock price right after the IPO.

Here’s how it works:

- The bank is authorized to sell 15% more shares than actually exist in the offering

- If the stock price rises (hot IPO), the bank buys those extra shares from the company at the IPO price — everyone’s happy

- If the stock price falls, the bank uses the extra cash from those phantom shares to buy stock in the open market, which props up the price and protects new investors

Think of it as a price shock absorber for the first few weeks of trading. It protects the company’s reputation and the early investors from a stomach-dropping first week.

The name for the overeallotment option comes from the Green Shoe Manufacturing Company, which was the first company to allow this practice at its IPO in 1960.

Chapter 5. How Do You Get Shares in a Hot IPO?

To be honest: the deck is stacked against regular investors.

The banks allocate most shares before the stock even starts trading, and they go to:

- Big institutional investors: these include mutual funds, pension funds, hedge funds (they’re repeat customers with the Big Banks worth $$$ millions in future fees)

- Wealthy private clients of the bank: these clients typically have a minimum of $250,000 that they would be willing to wager on each IPO

- Company insiders and friends: this includes a short list of individuals and family offices with connections to employees and owners (current stock holders) of the private company stock

By the time a regular person can buy shares, the stock is already trading publicly — often at a significant premium to the IPO price. That’s why you hear about stocks “popping” 40% on opening day: those price gains mostly went to the insiders.

Ways an ordinary investor can participate:

- Brokerage allocations — some brokers (Fidelity, Schwab, Robinhood Markets) receive small allocations and pass them to good customers

- Wait for the dust to settle — often the smartest move is waiting 3–6 months until hype fades and you can buy at a rational price. In most cases there is a “Lock-Up” period where insiders CANNOT sell their shares on the open market. It is important to know those lock-ups (3 months, 6 months) so that you can time any purchases and not get burned yourself for bad timing.

- ETFs that hold recent IPOs — a diversified, lower-risk way to participate

Chapter 6. How Do Bankers Decide on the Price?

This is equal parts science and educated guessing.

The bankers look at:

- Comparable companies — if similar public companies trade at 20x their earnings, it could be that your company should trade near that valuation as well

- Growth rate — faster-growing companies command higher earnings multiples and higher prices (investors pay a premium for the future)

- The roadshow feedback — the investment bankers literally take orders from big investors they have exposed to the company and gauge demand (high/medium/low) before setting a final price

Two key terms worth knowing:

- Valuation is the total estimated worth of the company (like the appraised value of a house)

- Float is what percentage of the company is actually being sold to the public

Here’s the key insight on IPO Pricing: Bankers intentionally price IPOs slightly below what they think the market will pay. A stock that jumps 15%–20% on opening day makes everyone look good — the company got its money, the early investors are happy, and the big institutional buyers made an instant profit. A stock that falls on day one can be a ugly for everyone’s reputation, and the Investment Bankers are on the hook to handle the shares that did not sell.

Closing Thoughts for IPO Investors

An Initial Public Offering is fundamentally a company saying: “We’ve built something real. Now we want the public to own a piece of it — and we need their money to build something even bigger” (as noted in the Chapter 2 pie charts above). The whole machinery of banks, pricing, green shoes, and allocations exists to make that transfer of ownership as smooth and credible as possible.

Make no mistake about it, the game is rigged toward insiders, because it was designed to give insiders liquidity. That said, understanding how it works puts you miles ahead of most other future investors.

NOTE WELL: there are some additional IPO’s in the works this year – 2026 (Anthropic, Jersey Mike’s Subs, Kraken, Liquid Death, OpenAI, Oura, Seat Geek, Strava, and Shein for example). You should decide now how you want to play the IPO game. Figure out who the winners and losers are, if you think you are up to the challenge. In all IPOs there can be an overhang of excitement and FOMO; so beware that euphoria often clouds your thinking. Invest wisely and good luck!