Friday Finance: What is a Roth IRA vs. a Traditional IRA?

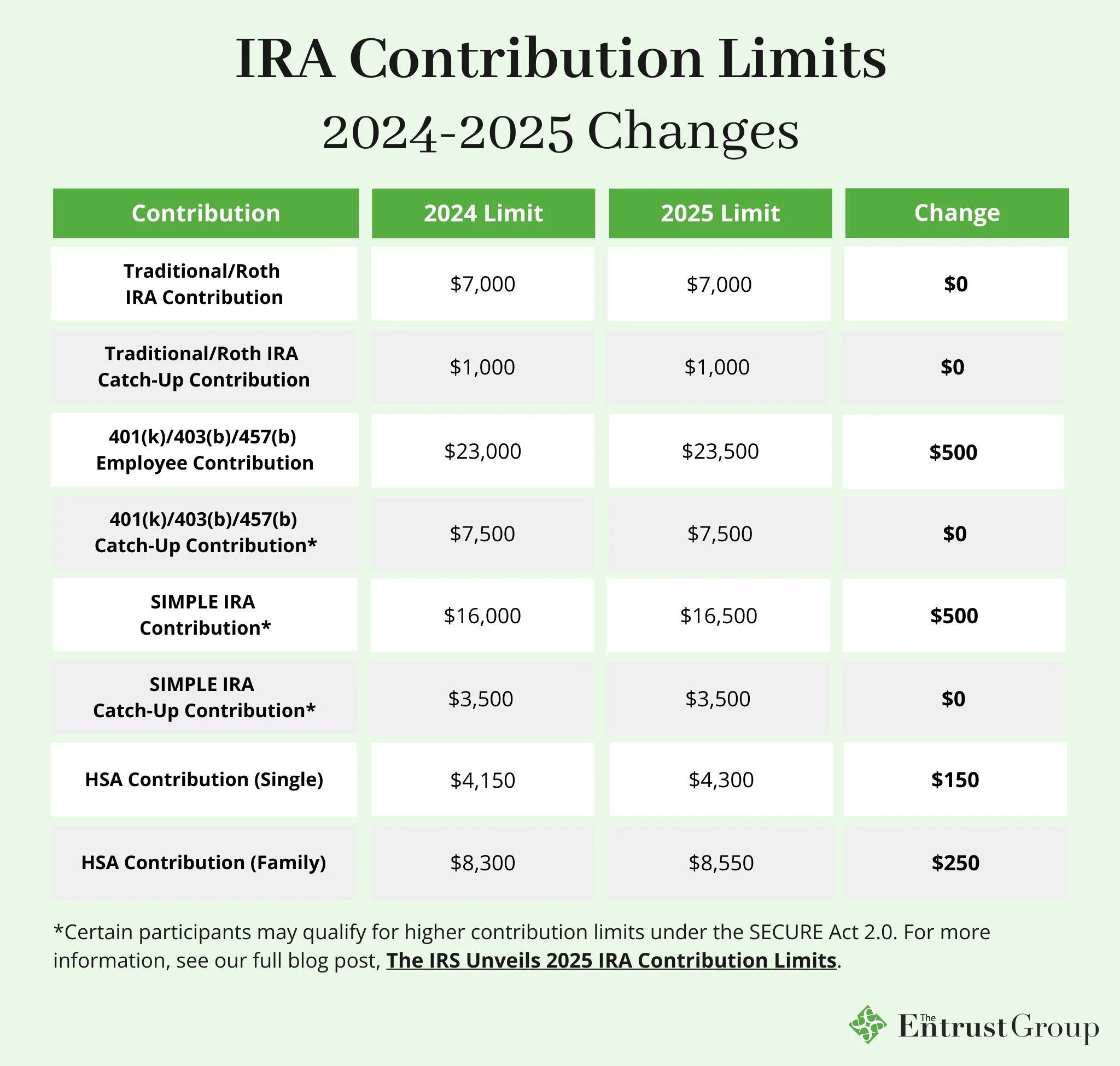

As you can tell from the slide above by The Entrust Group, there are a lot of IRA’s out there, Individual Retirement Accounts, that is. They are federally sponsored retirement savings plans. Figuring out what is right for you can get complicated. That said, I want this to be a simple and straight forward approach to saving for your future retirement, with specific withdrawal flexibility of a Roth.

The basics are that with a Roth or Traditional Plan you need to invest the money yourself. For beginners, start early, and test the waters. Going to a company like Fidelity, Schwab, Vanguard, or Robinhood can make the process of saving and investing easier on your time and relative interest in investing. You can invest all or some of the IRAs in the ETF’s, funds or individual stocks/bonds you want and watch it grow over time.

But First Who is Roth? And Should I Care?

Senator William V. Roth, Jr. was a U.S. Senator from Delaware who co-authored the legislation that created the eponymous Roth IRA. A Republican, Roth served in the Senate for three decades (1971-2001).

And YES, you should care about a Roth IRA, especially if you are a wage-earner in a lower tax bracket now than you expect to be when you hit retirement. The key difference between a Roth IRA and a Traditional IRA lies in when you pay taxes on your contributions and the FLEXIBILITY of pre-retirement withdrawals with the Roth vs a Tradtional IRA.

A Roth IRA is funded with after-tax dollars, offering tax-free withdrawals in retirement, while a Traditional IRA is funded with pre-tax dollars, providing an upfront tax deduction but taxing withdrawals in retirement. The choice depends on whether you’d rather pay taxes now (Roth) for tax-free withdrawals later, or pay taxes later (Traditional) for a tax break now. (There are also Roth Conversions, which shift assets from Traditional IRA’s to Roth’s, but that is better understood and navigated on a case-by-case basis).

Here’s a breakdown of the key differences:

Roth IRA

- Contributions: Made with after-tax dollars; not deductible in the current year. You or your spouse must be earning an income to put money into a Roth. There are specific rules for a “spousal Roth” which you may want to investigate with your spouse.

- Growth: Your money grows tax-free for as long as you want it to exist.

- Withdrawals: Qualified withdrawals in retirement are completely tax-free, provided the account has been open for at least five years and you are at least 59½.

- Required Minimum Distributions (RMDs): There are no RMDs during the original owner’s lifetime.

- Best For: People who expect to be in a higher tax bracket in retirement than they are currently.

Traditional IRA

- Contributions: Made with pre-tax dollars, potentially making them tax-deductible in the current year.

- Growth: Your money grows tax-deferred for as long as it exists. (Note: a Traditional IRA is tax-deferred, while a Roth is tax-free.)

- Withdrawals: Funds are taxed as ordinary income (not as capital gains) when withdrawn in retirement. There are tax penalties on early withdrawal of Traditional IRAs, so learn the rules.

- RMDs: Required distributions generally begin at age 73 and follow a set pattern of distributions and taxes on those assets. Again, you are taxed with the RMDs as ordinary income.

- Best For: People who want a tax break now and expect to be in the same or a lower tax bracket in retirement.

Choosing the Right IRA for you

- Current vs. Future Tax Bracket: This is the primary factor. If you expect your income (and tax bracket) to be higher in retirement, a Roth IRA is often better. If you expect your income to be lower in retirement, a Traditional IRA may be more beneficial. This can be tricky, as each administration has the ability to juggle these brackets to serve the American public as they see fit.

- Income Limitations: There are income caps for contributing to a Roth IRA, while Traditional IRAs are more accessible, though deductibility can be limited by income if you have a workplace retirement plan.

- Flexibility: Roth IRAs allow you to withdraw contributions (but not earnings) at any time, for any reason, without taxes or penalties. This feature is handy, if you need a Roth as a college savings plan, downpayment plan, or if your withdrawal lies in the other extraordinary expense category.