Friday Finance: A Corp

Colorado’s proposed “A Corp” — more formally the Artist Corporation or Artist Company under the proposed “Colorado Artist Company Act” (SB 26-133) — is essentially a specialized form of LLC designed specifically for artists and creators. It is not a traditional “corporation” in the same sense as a C corp or S corp. To use an overused disclaimer of “transparency” my daughter, Kathleen Hooper, is a musical professional. Nonetheless, these artists are overly burdened by the current business situation.

The idea behind the new business categorisation is that ordinary business entities were built for conventional commercial enterprises, not for people whose main assets are:

- intellectual property,

- creative control,

- royalties,

- collaborative authorship,

- and artistic mission.

The A-Corp attempts to solve those problems structurally.

What an A-Corp actually is

Legally, it is:

- an LLC-like entity created under Colorado statute,

- with mandatory artist protections built into the law itself,

- rather than relying on expensive custom contracts.

The legislation calls these “Artist Companies.”

Core features

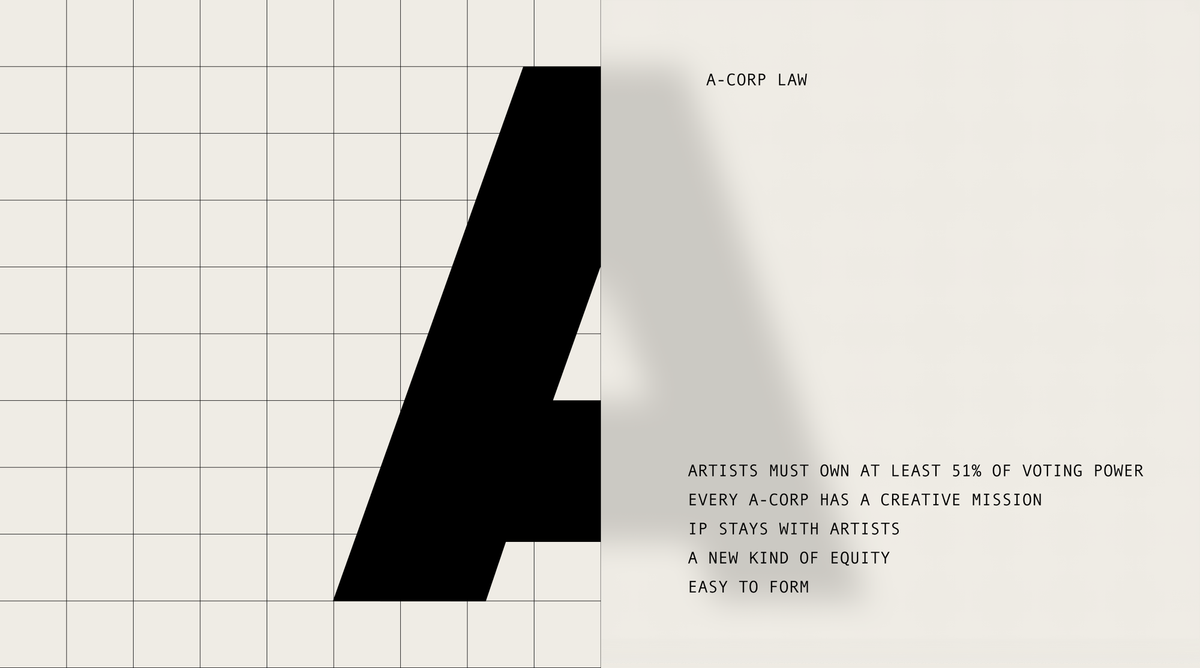

1. Artists must retain control

The defining feature is:

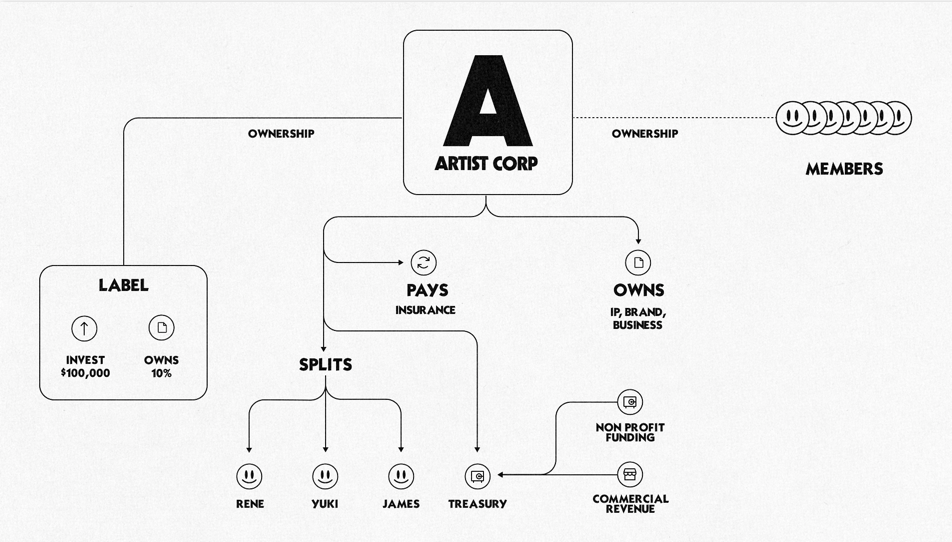

Artists must own at least 51% of the voting control.

That requirement cannot simply be contracted away in the operating agreement.

Why this matters

In many traditional entertainment or startup arrangements:

- investors can eventually control the company,

- catalogs can be sold,

- artists lose decision-making power.

The A-Corp is designed to prevent that.

Example

A musician could:

- sell economic participation to investors,

- but still legally maintain creative governance.

2. Artistic mission becomes legally recognized

Every A-Corp must declare an artistic mission in its founding documents.

That mission can:

- take precedence over profit,

- be equal to profit,

- or be balanced in a specified way.

This resembles the philosophy behind a Benefit Corporation (“B Corp”), but specifically focused on artistic purpose.

Example

An independent film collective might state:

“To create experimental documentary cinema preserving indigenous oral histories.”

That mission gains legal significance in governance.

3. Intellectual property protections

One of the most novel elements:

If the company dissolves, the artistic IP reverts back to the artists rather than automatically becoming available to creditors or outside investors.

This is a major departure from ordinary business entities.

Why that matters

Under conventional structures:

- masters,

- catalogs,

- scripts,

- publishing rights,

- trademarks,

- game assets,

may be sold during bankruptcy or liquidation.

The A-Corp tries to preserve creator ownership.

4. Separation of economic rights from governance rights

The law allows:

- investors to receive economic benefits,

while - artists keep voting and creative authority.

This is somewhat analogous to:

- dual-class stock structures at tech firms,

but tailored to artists.

Example

Fans or investors could:

- buy revenue participation,

- receive royalties,

- share profits,

without controlling:

- artistic direction,

- licensing decisions,

- or creative personnel.

5. “A-Corp Shares”

The proposal introduces a special ownership concept sometimes called “A-Corp Shares.”

These shares are intended to:

- recognize creative contribution as capital,

- allow fractional ownership,

- facilitate collaborative authorship.

Example

A game studio could allocate ownership to:

- programmers,

- writers,

- composers,

- artists,

- designers,

based on creative contribution rather than only cash investment.

Who it is best suited for

Potentially very attractive for:

| Type of creator | Why |

|---|---|

| Musicians | Protect catalogs and masters |

| Film collectives | Shared ownership of IP |

| Indie game studios | Collaborative creative equity |

| Writers’ groups | IP retention |

| Digital creators | Audience investment without loss of control |

| Art cooperatives | Governance flexibility |

| Creative startups | Raise capital while protecting mission |

What it is not

It is not:

- a replacement for copyright law,

- a tax loophole,

- a federal tax classification,

- or a standard corporation under IRS Subchapter A/B/C/S.

The “A” is essentially branding for “Artist.”

Tax treatment would likely resemble LLC taxation unless elections are made otherwise. The structure is primarily about:

- governance,

- ownership,

- and IP rights,

not tax engineering.

Main advantages

Stronger creator control

Probably the biggest feature.

Better IP protection

Catalogs and creative assets remain tied to creators.

Easier collaboration

Especially for modern decentralized creative teams.

More investor flexibility

Can attract funding without surrendering control.

Standardized legal framework

Avoids expensive bespoke contracts.

Potential downsides and criticisms

Investors may dislike limited control

Traditional venture capital and entertainment financing often depends on governance rights.

Some investors may hesitate.

Unproven legally

This is brand-new territory.

Courts have not yet extensively interpreted these provisions.

Interstate uncertainty

Other states may not initially recognize every feature seamlessly.

Could complicate financing

Banks and institutional investors generally prefer conventional structures.

Possible governance ambiguity

Balancing “mission” and profit can become legally messy.

Current status

As of May 2026:

- Colorado appears poised to become the first state to authorize the structure,

- the bill passed the legislature,

- and Governor Jared Polis is expected to sign it.

The law would take effect in 2026–2027 depending on implementation timelines.

The bigger significance

The proposal is actually fairly ambitious philosophically.

It attempts to treat:

- artistic labor,

- authorship,

- and cultural production

as deserving a specialized legal infrastructure — similar to how:

- cooperatives,

- nonprofits,

- LLCs,

- and Benefit Corporations

were created for different economic realities. The creators of the proposal openly describe it as: a business entity built for the “creative century.”